Fireflies.ai: why it broke out, what exactly happened, and how it stacks up (with numbers)

The inside story of timing, product-led growth, and agentic AI apps that turned a simple meeting bot into one of the most successful players in the AI collaboration space.

TL;DR

Fireflies’ success is the result of well-timed product-led growth (PLG) riding two macro waves: the 2020 remote-meeting boom and the 2023–2025 generative-AI upgrade cycle. The team paired a low-friction “bot joins your calendar meetings” distribution model with cross-platform coverage (Zoom/Meet/Teams), sticky integrations, and—more recently—agentic AI “apps” that turn notes into actions. As of mid-2025, Fireflies claims 20M people, 500k+ organizations, usage at 75% of the Fortune 500, and a $1B valuation following a tender offer; pricing starts at $10/seat annually (Pro) and $19/seat annually (Business), undercutting many peers. (Fireflies.ai)

What actually happened (the timeline & inflection points)

2016–2019: groundwork + PLG DNA

Founded by Krish Ramineni and Sam Udotong (both ex-Microsoft/MIT lineage), Fireflies spent several years building the core “AI notetaker joins calls, transcribes, and organizes” loop. Early messaging emphasized speed to value: invite a bot ([email protected]) and get searchable transcripts + highlights. (MIT News, Fireflies.ai)

2020–2021: the remote-meeting explosion

In weeks, Zoom went from 10M to 300M daily meeting participants (Google Meet and Microsoft Teams also spiked). Tools that captured and structured meeting content suddenly had a massive top-of-funnel. Fireflies rode this surge with a calendar-autojoin bot and coverage across Zoom/Meet/Teams, which mattered because companies were often using more than one platform. (Zoom, Business of Apps, DemandSage)

Press/features at the time (e.g., MIT) spotlighted Fireflies as a virtual assistant (“Fred”) that joins calls and sends searchable transcripts and notes after, reinforcing the “it just works” PLG motion. (MIT News)

2021: capital to scale

Fireflies raised Series A (widely reported as led by Khosla), coinciding with broad category validation (sales intelligence recorders, AI note-takers, etc.).* (Fireflies.ai)

2023–2025: from notes → actions (agentic AI)

Fireflies leaned into LLMs: AskFred to query meetings; a Chrome extension for real-time Meet transcripts; and in April 2025, it launched “200+ agentic AI apps” that tailor outputs (e.g., sales/recruiting-specific) and trigger post-meeting workflows. This shifted the value prop from “transcribe & summarize” to “summarize & do things.” (Fireflies.ai, Business Wire, Yahoo Finance)

June 12, 2025: Fireflies announced a >$1B valuation after a tender offer and claimed 20M users in 500k+ organizations (with presence at 75% of Fortune 500). It also revealed a Perplexity partnership (“Talk to Fireflies”) to inject live web knowledge into meetings—again, pushing beyond transcription. (Fireflies.ai)

* (Funding totals vary by source; third-party dossiers list ~$19M raised over multiple rounds, and earlier seed/convertible raises in 2017–2019.) (Clay)

The growth engine (why it worked)

Frictionless capture → PLG virality

The “bot joins your meetings” model piggybacks on your calendar—no heavy IT rollout required—and quietly introduces Fireflies to every attendee on the invite. That’s textbook PLG distribution. The later Chrome extension reduced friction further for Google Meet. (Fireflies.ai)

Cross-platform + ecosystem integrations

Many companies use Zoom and Meet and Teams. Fireflies covers all and pushes outputs into CRMs, project tools, and docs via 60+ native integrations (plus Zapier/Make). That turns notes into work artifacts and raises switching costs. (Fireflies.ai, Zapier, Make)

Generous pricing vs. value

Public pricing undercuts many peers: Pro at $10/seat (annually), Business at $19/seat (annually); Enterprise $39/seat adds SSO, HIPAA, private storage, etc. That’s a compelling entry for teams, particularly compared with enterprise sales-intel suites. (Fireflies.ai)

Brand/social proof & trust

Fireflies markets GDPR/SOC 2 and a Trust Center (with SOC 2 report/mNDA), plus high user ratings (G2 4.8/5 with ~700+ reviews reported by several trackers), which grease security reviews and mid-market adoption. (Fireflies.ai, G2)

Category evolution: from commodity text → “agentic” outcomes

The 2025 AI Apps launch (200+ apps) reframes Fireflies as a workflow product: summarizing by role, writing follow-up emails, updating CRMs, creating scorecards, etc.—a defense against commoditized transcription/summaries now built into Zoom and Teams. (Business Wire, Fireflies.ai)

The role of timing

Pandemic spike (2020): A once-in-a-generation demand shock in virtual meetings created an enormous funnel. Zoom alone jumped to 300M daily participants by April 2020 (from 10M), while Teams/Meet also surged. Fireflies’ “autojoin bot + cross-platform coverage” slotted right in. (Zoom, Business of Apps, DemandSage)

Gen-AI step-change (2023–2025): LLMs made it feasible to go beyond transcripts to usable, structured summaries with actions, and Fireflies pushed further with agentic apps and Perplexity search in meetings. That evolution matters as Zoom and Microsoft now ship native AI notes—third-party tools must do more than transcribe. (Business Wire, Zoom Support, TECHCOMMUNITY.MICROSOFT.COM)

Numbers snapshot (as of mid-2025)

Users & customers: 20M+ people, 500k+ organizations; used at 75% of the Fortune 500 (company claim, June 12, 2025). (Fireflies.ai)

Valuation: >$1B (tender offer announced June 12, 2025). (Fireflies.ai)

Agentic app ecosystem: 200+ AI apps shipping actions/outcomes by department. (Business Wire)

Integrations: 60+ native (plus Zapier/Make). (Fireflies.ai, Make)

Pricing (public): Pro $10/seat annually, Business $19/seat annually, Enterprise $39/seat annually; monthly options are higher. (Fireflies.ai)

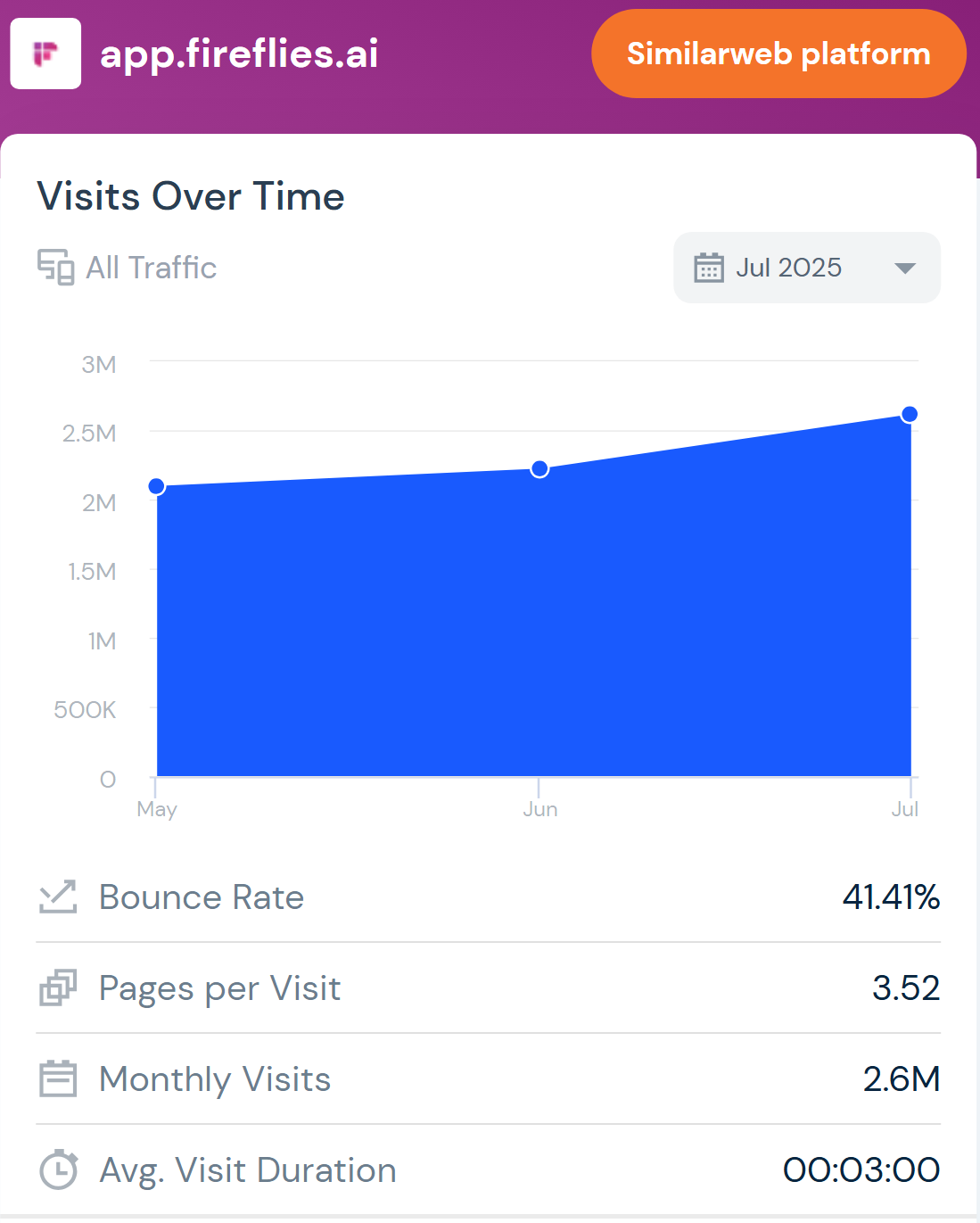

Traffic (directional): Similarweb shows ~3.5M monthly visits recently; take with caution as it reflects web traffic, not product MAUs. (Similarweb)

Team size: ~100–110+ employees (3rd-party directories; directional). (LeadIQ)

3rd-party ARR estimate (caveat): Latka/aggregators peg ~$10.9M revenue and ~35k paying customers in 2024—likely understating current scale given the 2025 user claims; treat as rough. (Latka)

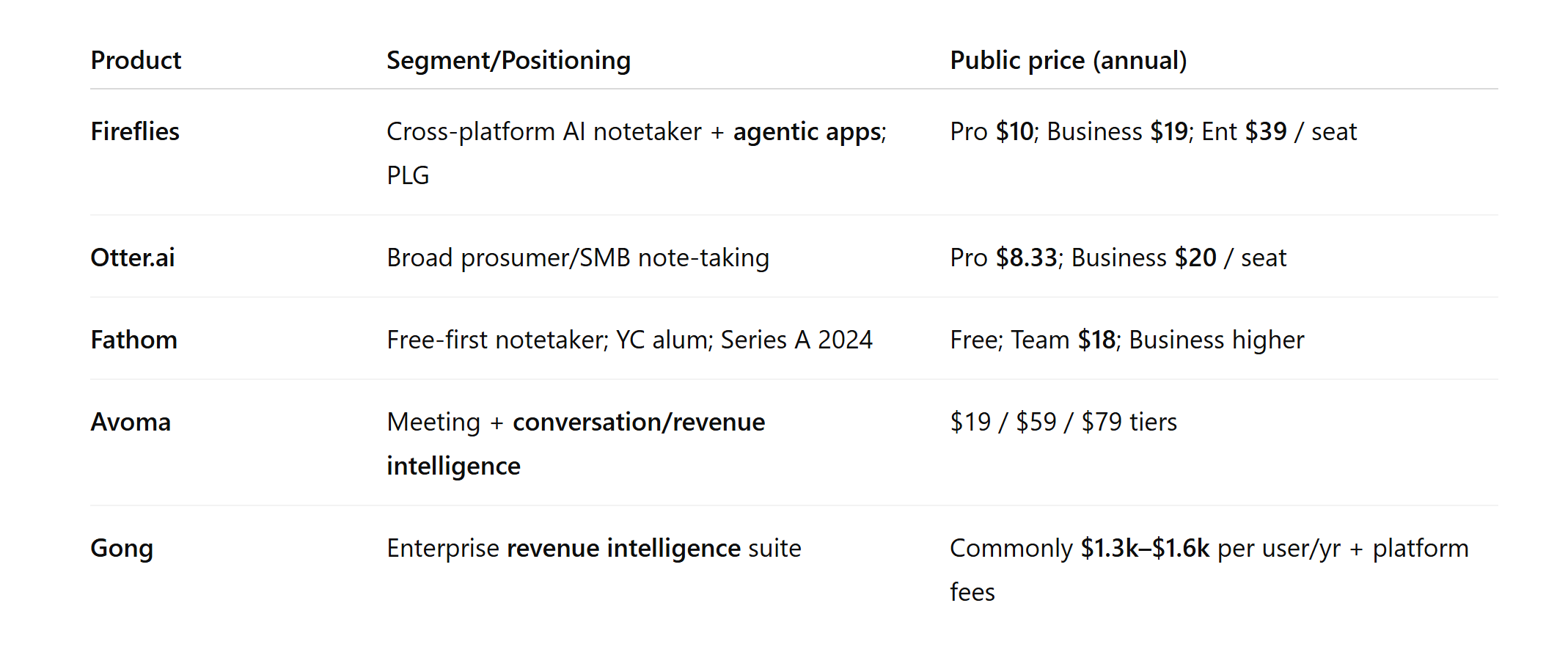

How Fireflies compares (pricing & scale)

short table (just the essentials; prose lives outside the table)

Adoption & scale markers

Fireflies: company-claimed 20M users / 500k orgs, 75% F500 presence; G2 4.8/5 rating (hundreds of reviews); “agentic apps” angle is unique at this breadth. (Fireflies.ai, G2)

Otter.ai: broader brand awareness with ~$100M ARR (Mar 2025, Fortune), strong consumer/SMB footprint, expanding language support and feature set. (Fireflies.ai, Lifewire)

Fathom: $17M Series A (Sep 2024); growing fast on a freemium model (unlimited recordings for individuals). (TechCrunch)

Avoma: priced for teams needing analytics/CI/RI; 3rd-party estimates suggest low- to mid-eight-figure revenue. (Growjo)

Gong: dominant enterprise CI/RI; far more expensive and heavier deployment; not a direct alternative for “notes only,” but overlaps on sales-call capture. (Gong, Claap)

Product angle

Native platforms (Zoom AI Companion, Microsoft Copilot) now include summaries/notes, which compresses the “transcribe & summarize” wedge. Fireflies’ cross-platform coverage and post-meeting automations (apps, CRM syncs) are its counter-move. (Zoom Support, TECHCOMMUNITY.MICROSOFT.COM)

Why Fireflies got traction while others stalled

Distribution nailed early: The calendar-autojoin bot minimized setup friction and created built-in virality (every attendee sees it), while the Chrome extension removed bot friction on Google Meet. This is a classic PLG flywheel in a category where adoption usually dies on IT approval. (Fireflies.ai)

Cross-platform as a moat: Many teams straddle Zoom/Meet/Teams; Fireflies works across all and pushes results into 60+ integrations, so it becomes the system of record for conversations, not just a Zoom feature. (Fireflies.ai)

Pricing vs. value: Public, low entry prices (with “unlimited” transcription on paid tiers) lower the barrier for teams to standardize on one tool even when Zoom/Teams offer “good enough” notes. (Fireflies.ai)

Moving up the stack: The 200+ agentic AI apps let Fireflies differentiate on outcomes (emails, scorecards, CRM updates, role-tailored insights) instead of raw ASR accuracy, which is increasingly commoditized. (Business Wire)

Trust & social proof: G2 4.8/5 rating and compliance messaging (GDPR/SOC 2, HIPAA for Enterprise) reduce buyer anxiety—important as privacy scrutiny around AI notetakers has grown. (G2, Fireflies.ai)

Headwinds & risks (and how Fireflies is addressing them)

Platform encroachment: Zoom and Microsoft now ship native AI summaries; default wins unless a third-party adds cross-suite value or richer downstream automations. Fireflies’ agentic apps, Perplexity partnership, and deep integrations are meant to keep it indispensable. (Zoom Support, TECHCOMMUNITY.MICROSOFT.COM, Fireflies.ai)

Commoditization of transcription/summaries: As ASR/LLMs get cheaper and better, differentiation must be in workflows, security, and data gravity—hence the push into role-tailored outputs and enterprise controls (SSO, HIPAA, private storage) at the Enterprise tier. (Fireflies.ai)

Privacy optics: Media has noted awkward “AI notetaker” moments; robust consent flows and clear indicators are now table stakes. (Zoom’s own help docs stress how summaries are handled.) Fireflies’ Trust Center/SOC 2 positioning helps but isn’t a silver bullet. (The Wall Street Journal, Zoom Support)

Bottom line (my read)

Success drivers: lightning-in-a-bottle timing (2020), savvy PLG distribution, cross-platform surface area, and a fast pivot from commodity transcription to agentic workflows. The $1B valuation and 20M user claim reflect strong momentum, though revenue estimates from third-party trackers suggest a very large free/low-ARPU base—consistent with PLG dynamics in this category. (Fireflies.ai, Latka)

Competitive posture: Fireflies is strong vs. pure note-takers (price/features), but must keep out-innovating platforms (Zoom/Copilot) by owning the cross-platform, post-meeting workflow and making “notes → actions” the core value. (Zoom Support, TECHCOMMUNITY.MICROSOFT.COM)

Sources & key references

Fireflies milestones, users, valuation, agentic apps: company blog/press (Jun 12, 2025 valuation; Apr 23, 2025 AI Apps/agentic press). (Fireflies.ai, Business Wire)

Pricing (official): Fireflies pricing & help docs (2025). (Fireflies.ai, Fireflies)

Integrations: Fireflies integrations page; Make/Zapier pages. (Fireflies.ai, Make, Zapier)

Founding & early positioning: MIT News profile (May 21, 2020). (MIT News)

Market timing context (meeting growth): Zoom blog; Business of Apps; DemandSage (Teams minutes). (Zoom, Business of Apps, DemandSage)

Competitor pricing & scale: Otter pricing (official) and ARR (Fortune); Fathom funding (TechCrunch); Avoma pricing (G2/Claap); Gong pricing (analyst roundups). (Otter.ai, Fireflies.ai, TechCrunch, G2, tl;dv)

Ratings/reviews: G2 seller & product pages (Fireflies ~4.8/5). (G2)

Traffic & headcount (directional): Similarweb; LeadIQ. (Similarweb, LeadIQ)

Quick competitive cheat-sheet (who to watch)

Zoom AI Companion / Microsoft Copilot — built-in, increasingly capable meeting notes & action items; huge distribution advantage inside their suites. If these become “good enough,” third-party tools must win on cross-platform coverage and automation depth. (Zoom Support, TECHCOMMUNITY.MICROSOFT.COM)

Otter.ai — massive brand & ARR; strong mobile; expanding language support; similar price points on Business. (Fireflies.ai, Otter.ai)

Fathom — fast-growing freemium (Series A 2024), good UX; individual-first motion that can land & expand into teams. (TechCrunch)

Avoma — if you need deeper conversation/revenue intelligence (beyond notes), Avoma competes by bundling CI/RI analytics at mid-market price tiers. (Claap)

Gong — not a note-taker direct comp; it’s an enterprise revenue platform with high per-seat and platform fees. Fireflies can co-exist (cheap notes) or be displaced by Gong if sales org standardizes on it. (tl;dv)

Conclusion

Fireflies.ai exemplifies product‑led growth amplified by perfect timing. Its frictionless calendar bot went viral just as the pandemic made remote meetings ubiquitous. By staying lean, offering generous pricing, and rapidly adopting generative AI, Fireflies transformed from a simple transcription service into a workflow automation platform valued at over $1 billion. In a crowded landscape with players like Otter, Fathom, Avoma and native AI summaries from Zoom and Microsoft, Fireflies’ cross‑platform coverage, agentic capabilities, and compliance posture remain its competitive moats. The company must continue innovating beyond transcription to maintain its lead, but its current momentum and adoption metrics suggest it has built a durable business.